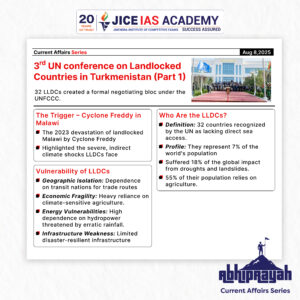

3rd UN conference on landlocked countries

UPSC CURRENT AFFAIRS – 08th August 2025 Home / 3rd UN conference on landlocked countries Why in News? At the

Issue of soapstone mining in Uttarakhand’s Bageshwar

UPSC CURRENT AFFAIRS – 08th August 2025 Home / Issue of soapstone mining in Uttarakhand’s Bageshwar Why in News? Unregulated

Groundwater Pollution in India – A Silent Public Health Emergency

UPSC CURRENT AFFAIRS – 08th August 2025 Home / Groundwater Pollution in India – A Silent Public Health Emergency Why

Universal banking- need and impact

UPSC CURRENT AFFAIRS – 08th August 2025 Home / Universal banking- need and impact Why in News? The Reserve Bank

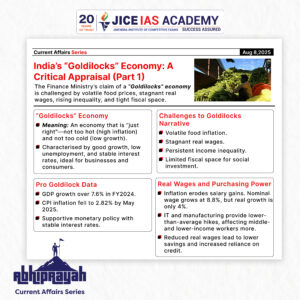

India’s “Goldilocks” Economy: A Critical Appraisal

UPSC CURRENT AFFAIRS – 08th August 2025 Home / India’s “Goldilocks” Economy: A Critical Appraisal Why in News? The Finance

U.S.-India Trade Dispute: Trump’s 50% Tariffs and India’s Oil Imports from Russia

UPSC CURRENT AFFAIRS – 07th August 2025 Home / U.S.-India Trade Dispute: Trump’s 50% Tariffs and India’s Oil Imports from

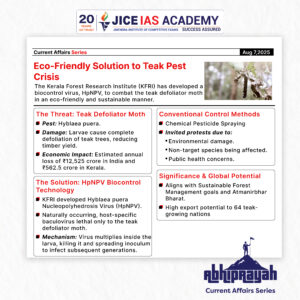

Eco-Friendly Solution to Teak Pest Crisis: KFRI’s HpNPV Technology

UPSC CURRENT AFFAIRS – 07th August 2025 Home / Eco-Friendly Solution to Teak Pest Crisis: KFRI’s HpNPV Technology Why in

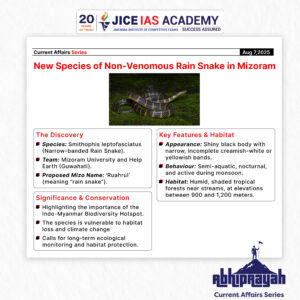

New Species of Non-Venomous Rain Snake Discovered in Mizoram

UPSC CURRENT AFFAIRS – 07th August 2025 Home / New Species of Non-Venomous Rain Snake Discovered in Mizoram Why in

Hello! I could have sworn I’ve been to this blog before but after browsing through some of the post I realized it’s new to me. Anyways, I’m definitely happy I found it and I’ll be book-marking and checking back frequently!

I have not checked in here for some time as I thought it was getting boring, but the last few posts are great quality so I guess I will add you back to my everyday bloglist. You deserve it my friend 🙂

I have not checked in here for some time because I thought it was getting boring, but the last several posts are good quality so I guess I will add you back to my everyday bloglist. You deserve it my friend 🙂

Very interesting info !Perfect just what I was looking for! “It’s the Brady Act taking manpower and crime-fighting capability off the streets.” by Dennis Martin.

Hmm is anyone else having problems with the images on this blog loading? I’m trying to find out if its a problem on my end or if it’s the blog. Any suggestions would be greatly appreciated.

I really like your writing style, excellent information, thanks for putting up : D.

Would love to always get updated outstanding weblog! .

Hello there, You have done an excellent job. I will certainly digg it and personally suggest to my friends. I’m sure they’ll be benefited from this website.

Thank you for sharing superb informations. Your website is very cool. I’m impressed by the details that you have on this site. It reveals how nicely you perceive this subject. Bookmarked this website page, will come back for extra articles. You, my pal, ROCK! I found simply the information I already searched all over the place and just couldn’t come across. What a great site.

A person essentially help to make seriously articles I would state. This is the first time I frequented your website page and thus far? I amazed with the research you made to make this particular publish amazing. Fantastic job!

I was suggested this website by my cousin. I’m not sure whether this post is written by him as no one else know such detailed about my problem. You are incredible! Thanks!

Good write-up, I?¦m normal visitor of one?¦s website, maintain up the excellent operate, and It’s going to be a regular visitor for a lengthy time.

Hello my loved one! I wish to say that this post is awesome, nice written and come with approximately all significant infos. I would like to look extra posts like this .

You actually make it seem really easy along with your presentation however I in finding this matter to be actually one thing that I feel I would never understand. It kind of feels too complex and very wide for me. I am having a look forward in your subsequent post, I¦ll try to get the cling of it!

Thank you for another fantastic post. Where else could anyone get that type of info in such an ideal way of writing? I have a presentation next week, and I’m on the look for such information.

Some really good info , Glad I observed this.

I truly enjoy reading on this website , it holds wonderful articles. “The secret of eternal youth is arrested development.” by Alice Roosevelt Longworth.

This website is my intake, rattling superb design and style and perfect subject material.

The Pink Salt Trick is a minimalist but effective morning routine: Just drink a glass of lukewarm water mixed with a pinch of Himalayan pink salt as soon as you wake up.

fantastic points altogether, you just gained a brand new reader. What might you recommend in regards to your put up that you simply made a few days ago? Any sure?

The Pink Salt Trick is a minimalist but effective morning routine: Just drink a glass of lukewarm water mixed with a pinch of Himalayan pink salt as soon as you wake up.

I truly wanted to send a brief message to express gratitude to you for those fabulous points you are giving here. My extended internet lookup has at the end been rewarded with sensible know-how to talk about with my family and friends. I ‘d state that that we website visitors actually are unquestionably endowed to exist in a notable network with very many brilliant professionals with very helpful techniques. I feel very blessed to have come across your entire website and look forward to some more excellent times reading here. Thanks a lot again for everything.

Throughout this great design of things you actually get a B- just for effort. Where you actually misplaced me ended up being in all the facts. As people say, the devil is in the details… And that could not be much more true here. Having said that, allow me say to you exactly what did work. The authoring is quite powerful which is most likely the reason why I am making the effort in order to opine. I do not make it a regular habit of doing that. 2nd, although I can certainly notice a leaps in reasoning you make, I am not certain of just how you appear to unite the points which in turn help to make the actual conclusion. For right now I will, no doubt yield to your point but wish in the near future you actually connect your facts much better.

Way cool, some valid points! I appreciate you making this article available, the rest of the site is also high quality. Have a fun.

The Pink Salt Trick is a minimalist but effective morning routine: Just drink a glass of lukewarm water mixed with a pinch of Himalayan pink salt as soon as you wake up.

Hiya, I’m really glad I’ve found this info. Nowadays bloggers publish just about gossips and internet and this is really irritating. A good blog with exciting content, this is what I need. Thank you for keeping this site, I will be visiting it. Do you do newsletters? Can not find it.

Wohh precisely what I was looking for, appreciate it for posting.

I genuinely enjoy looking through on this website , it holds fantastic articles.

Magnificent beat ! I wish to apprentice while you amend your web site, how can i subscribe for a blog site? The account aided me a acceptable deal. I had been tiny bit acquainted of this your broadcast offered bright clear concept

Enjoyed reading through this, very good stuff, regards. “It requires more courage to suffer than to die.” by Napoleon Bonaparte.

I think this is among the most significant information for me. And i’m glad reading your article. But should remark on few general things, The website style is perfect, the articles is really nice : D. Good job, cheers

Some truly nice and utilitarian info on this internet site, as well I conceive the layout contains good features.

Utterly indited content material, Really enjoyed reading.

Can I just say what a relief to find someone who actually knows what theyre talking about on the internet. You definitely know how to bring an issue to light and make it important. More people need to read this and understand this side of the story. I cant believe youre not more popular because you definitely have the gift.

Utterly composed subject material, thank you for information. “In the fight between you and the world, back the world.” by Frank Zappa.

I really like your writing style, excellent information, thank you for posting :D. “Silence is more musical than any song.” by Christina G. Rossetti.

I’ve recently started a website, the info you offer on this website has helped me greatly. Thank you for all of your time & work. “There is a time for many words, and there is also a time for sleep.” by Homer.

I love the efforts you have put in this, appreciate it for all the great posts.

Your place is valueble for me. Thanks!…

Pretty! This was a really wonderful post. Thank you for your provided information.

Some really nice stuff on this site, I like it.

obviously like your web site but you need to check the spelling on quite a few of your posts. Several of them are rife with spelling problems and I find it very bothersome to inform the truth however I¦ll surely come again again.

I believe you have mentioned some very interesting details , thankyou for the post.

Keep up the wonderful piece of work, I read few articles on this site and I conceive that your blog is rattling interesting and contains circles of great information.

Heya i’m for the first time here. I found this board and I find It really useful & it helped me out a lot. I am hoping to give something back and aid others like you helped me.

There is obviously a lot to identify about this. I feel you made various good points in features also.

Your place is valueble for me. Thanks!…

Incredible! This blog looks just like my old one! It’s on a totally different topic but it has pretty much the same page layout and design. Superb choice of colors!

Wow, awesome blog format! How lengthy have you been running a blog for? you made blogging glance easy. The overall look of your web site is excellent, as smartly as the content!

I’m usually to blogging and i really respect your content. The article has actually peaks my interest. I’m going to bookmark your web site and maintain checking for brand spanking new information.

I always was interested in this subject and still am, regards for putting up.

Saved as a favorite, I really like your blog!

Respect to post author, some wonderful information .

Good write-up, I?¦m normal visitor of one?¦s website, maintain up the nice operate, and It is going to be a regular visitor for a lengthy time.

F*ckin’ tremendous things here. I’m very glad to look your article. Thank you so much and i am having a look ahead to touch you. Will you please drop me a e-mail?

obviously like your web site but you need to test the spelling on quite a few of your posts. A number of them are rife with spelling problems and I in finding it very troublesome to tell the reality nevertheless I’ll certainly come again again.

hi!,I love your writing so so much! percentage we keep up a correspondence extra about your post on AOL? I need an expert on this house to unravel my problem. Maybe that’s you! Having a look ahead to look you.

Thank you for another informative blog. Where else could I get that kind of info written in such a perfect way? I’ve a project that I’m just now working on, and I’ve been on the look out for such information.

I like this weblog very much so much superb info .

Definitely consider that which you stated. Your favourite justification seemed to be at the web the simplest thing to remember of. I say to you, I definitely get irked while folks consider issues that they plainly do not know about. You controlled to hit the nail upon the top as smartly as defined out the whole thing without having side effect , folks can take a signal. Will likely be back to get more. Thank you

Pretty part of content. I simply stumbled upon your blog and in accession capital to claim that I get in fact enjoyed account your blog posts. Any way I’ll be subscribing to your augment or even I fulfillment you get entry to consistently rapidly.

I’ve been surfing on-line more than 3 hours these days, yet I never discovered any attention-grabbing article like yours. It is lovely value sufficient for me. In my opinion, if all site owners and bloggers made excellent content as you probably did, the internet will probably be a lot more helpful than ever before.

Wohh exactly what I was searching for, thankyou for putting up.

I’ve recently started a website, the information you offer on this website has helped me tremendously. Thanks for all of your time & work. “A creative man is motivated by the desire to achieve, not by the desire to beat others.” by Ayn Rand.

osfo43

What’s Happening i am new to this, I stumbled upon this I’ve found It positively helpful and it has aided me out loads. I hope to contribute & help other users like its helped me. Good job.

Hi there, You’ve done an excellent job. I will certainly digg it and individually suggest to my friends. I’m confident they will be benefited from this site.

Wow! Thank you! I constantly wanted to write on my site something like that. Can I take a part of your post to my site?

Wonderful web site. Lots of useful info here. I?¦m sending it to some pals ans additionally sharing in delicious. And obviously, thanks in your effort!

You made some good points there. I did a search on the subject and found most guys will go along with with your blog.

Its excellent as your other blog posts : D, regards for posting. “I catnap now and then, but I think while I nap, so it’s not a waste of time.” by Martha Stewart.

This blog is definitely rather handy since I’m at the moment creating an internet floral website – although I am only starting out therefore it’s really fairly small, nothing like this site. Can link to a few of the posts here as they are quite. Thanks much. Zoey Olsen

Terrific work! This is the type of information that should be shared around the web. Shame on the search engines for not positioning this post higher! Come on over and visit my website . Thanks =)

It’s in point of fact a great and helpful piece of information. I’m satisfied that you simply shared this useful info with us. Please keep us informed like this. Thank you for sharing.

whoah this blog is great i love reading your articles. Keep up the great work! You know, a lot of people are looking around for this information, you can help them greatly.

Hi there, I found your web site via Google while searching for a comparable subject, your site got here up, it looks great. I have bookmarked it in my google bookmarks.

Flash Burn is a revolutionary natural supplement that has been transforming the lives of thousands of people struggling with excess weight. Developed with a 100 natural and scientifically proven formula

The Pink Salt Trick is a minimalist but effective morning routine: Just drink a glass of lukewarm water mixed with a pinch of Himalayan pink salt as soon as you wake up.

What i don’t realize is actually how you’re not actually much more well-liked than you may be now. You’re so intelligent. You realize therefore considerably relating to this subject, made me personally consider it from so many varied angles. Its like men and women aren’t fascinated unless it’s one thing to accomplish with Lady gaga! Your own stuffs nice. Always maintain it up!

Hey There. I found your blog using msn. That is a very well written article. I’ll make sure to bookmark it and return to read more of your useful info. Thank you for the post. I’ll certainly comeback.

Along with every thing that appears to be building throughout this specific area, all your perspectives happen to be quite radical. However, I appologize, but I do not give credence to your whole plan, all be it radical none the less. It looks to us that your commentary are generally not completely validated and in actuality you are generally your self not fully confident of the assertion. In any event I did take pleasure in reading it.

Good ?V I should definitely pronounce, impressed with your web site. I had no trouble navigating through all the tabs as well as related information ended up being truly easy to do to access. I recently found what I hoped for before you know it at all. Quite unusual. Is likely to appreciate it for those who add forums or something, site theme . a tones way for your customer to communicate. Nice task..

Excellent read, I just passed this onto a friend who was doing some research on that. And he just bought me lunch as I found it for him smile So let me rephrase that: Thank you for lunch! “The future is not something we enter. The future is something we create.” by Leonard I. Sweet.

I’m not positive the place you’re getting your information, but good topic. I must spend a while learning much more or working out more. Thank you for magnificent information I used to be searching for this info for my mission.

Some really interesting info , well written and generally user genial.

Keep working ,impressive job!

Respect to article author, some superb selective information.

I really enjoy looking through on this website, it has got good content. “Never fight an inanimate object.” by P. J. O’Rourke.

Simply desire to say your article is as astounding. The clarity for your post is just great and i can assume you’re knowledgeable in this subject. Fine along with your permission allow me to grab your RSS feed to keep updated with approaching post. Thanks one million and please carry on the enjoyable work.

We are a group of volunteers and opening a new scheme in our community. Your web site offered us with valuable information to work on. You’ve done an impressive job and our entire community will be grateful to you.

I believe other website proprietors should take this website as an example , very clean and excellent user friendly style and design.

I couldn’t resist commenting

It’s arduous to find knowledgeable folks on this topic, however you sound like you know what you’re talking about! Thanks

I gotta bookmark this website it seems very useful invaluable

Thank you, I’ve just been looking for info about this subject for ages and yours is the best I have discovered so far. But, what about the conclusion? Are you sure about the source?

I intended to draft you a very little word just to give many thanks the moment again for your great knowledge you’ve featured on this site. It was so tremendously generous with you to offer publicly precisely what numerous people might have offered for sale as an ebook to make some dough on their own, specifically considering that you could possibly have tried it in the event you desired. Those basics likewise served like a fantastic way to be sure that other people online have the identical desire the same as my own to grasp a whole lot more with reference to this condition. I’m certain there are millions of more fun instances in the future for many who read carefully your site.

I really like reading and I conceive this website got some genuinely utilitarian stuff on it! .

Thankyou for this post, I am a big fan of this site would like to continue updated.

It is perfect time to make some plans for the future and it’s time to be happy. I have learn this put up and if I may I wish to recommend you few fascinating issues or advice. Perhaps you can write next articles relating to this article. I want to read even more things about it!

I enjoy the efforts you have put in this, thank you for all the great articles.

excellent points altogether, you just gained a brand new reader. What would you recommend in regards to your post that you made some days ago? Any positive?

Hello my family member! I wish to say that this article is amazing, nice written and come with approximately all significant infos. I?¦d like to see more posts like this .

Some genuinely great content on this website , thankyou for contribution.

After I originally commented I clicked the -Notify me when new feedback are added- checkbox and now every time a remark is added I get four emails with the same comment. Is there any means you may remove me from that service? Thanks!

Hello. excellent job. I did not expect this. This is a impressive story. Thanks!

I am not sure the place you are getting your information, however good topic. I must spend some time studying much more or understanding more. Thank you for great information I was on the lookout for this info for my mission.

I am glad to be a visitor of this everlasting site! , regards for this rare info ! .

Precisely what I was looking for, thankyou for putting up.

This blog is definitely rather handy since I’m at the moment creating an internet floral website – although I am only starting out therefore it’s really fairly small, nothing like this site. Can link to a few of the posts here as they are quite. Thanks much. Zoey Olsen

What’s Happening i’m new to this, I stumbled upon this I’ve found It absolutely helpful and it has helped me out loads. I hope to contribute & assist other users like its aided me. Great job.

Hi my family member! I wish to say that this article is awesome, nice written and include approximately all vital infos. I would like to see more posts like this.

You are a very clever person!

This website is my aspiration, rattling wonderful design and perfect content.

I went over this website and I conceive you have a lot of great info, saved to my bookmarks (:.

Hello! Do you know if they make any plugins to protect against hackers? I’m kinda paranoid about losing everything I’ve worked hard on. Any tips?

Good website! I truly love how it is easy on my eyes and the data are well written. I am wondering how I might be notified when a new post has been made. I’ve subscribed to your RSS feed which must do the trick! Have a nice day!

I love the efforts you have put in this, regards for all the great blog posts.

We’re a gaggle of volunteers and starting a new scheme in our community. Your site offered us with helpful info to paintings on. You have performed a formidable task and our whole community shall be grateful to you.

I’m still learning from you, but I’m trying to reach my goals. I absolutely enjoy reading all that is posted on your blog.Keep the aarticles coming. I enjoyed it!

Some truly prime posts on this site, saved to bookmarks.

Some really terrific work on behalf of the owner of this web site, dead great subject material.

This is a topic close to my heart cheers, where are your contact details though?

In this awesome design of things you get an A just for hard work. Where exactly you confused me personally was first in your specifics. As it is said, the devil is in the details… And it couldn’t be much more accurate at this point. Having said that, allow me inform you precisely what did do the job. Your article (parts of it) is definitely very engaging which is possibly the reason why I am making an effort to comment. I do not really make it a regular habit of doing that. Secondly, although I can see the jumps in reason you make, I am definitely not sure of how you seem to unite the details which help to make your final result. For right now I will, no doubt yield to your issue however hope in the foreseeable future you link the dots much better.

Well I definitely enjoyed reading it. This article offered by you is very constructive for correct planning.

Thank you for some other magnificent post. Where else could anyone get that kind of information in such a perfect method of writing? I’ve a presentation next week, and I am at the look for such information.

hello there and thank you for your info – I’ve certainly picked up something new from right here. I did however expertise some technical points using this web site, since I experienced to reload the site lots of times previous to I could get it to load properly. I had been wondering if your web host is OK? Not that I am complaining, but sluggish loading instances times will very frequently affect your placement in google and could damage your quality score if advertising and marketing with Adwords. Anyway I am adding this RSS to my email and can look out for much more of your respective intriguing content. Ensure that you update this again soon..

I am constantly searching online for ideas that can benefit me. Thx!

Perfectly indited content material, Really enjoyed examining.

This design is wicked! You certainly know how to keep a reader entertained. Between your wit and your videos, I was almost moved to start my own blog (well, almost…HaHa!) Wonderful job. I really enjoyed what you had to say, and more than that, how you presented it. Too cool!

I went over this internet site and I believe you have a lot of good information, saved to bookmarks (:.

My coder is trying to persuade me to move to .net from PHP. I have always disliked the idea because of the expenses. But he’s tryiong none the less. I’ve been using Movable-type on various websites for about a year and am nervous about switching to another platform. I have heard excellent things about blogengine.net. Is there a way I can import all my wordpress content into it? Any help would be really appreciated!

I appreciate, cause I found just what I was looking for. You’ve ended my 4 day long hunt! God Bless you man. Have a nice day. Bye

It?¦s in point of fact a great and useful piece of information. I am glad that you shared this helpful info with us. Please keep us informed like this. Thank you for sharing.

Excellent web site. A lot of useful info here. I am sending it to a few friends ans also sharing in delicious. And naturally, thanks for your effort!

I’m impressed, I need to say. Really not often do I encounter a weblog that’s each educative and entertaining, and let me let you know, you have hit the nail on the head. Your idea is outstanding; the difficulty is something that not enough persons are speaking intelligently about. I am very completely satisfied that I stumbled across this in my seek for one thing referring to this.

You can certainly see your expertise in the paintings you write. The sector hopes for even more passionate writers such as you who are not afraid to say how they believe. All the time follow your heart.

This is the proper weblog for anybody who needs to search out out about this topic. You notice so much its almost onerous to argue with you (not that I truly would want…HaHa). You undoubtedly put a brand new spin on a topic thats been written about for years. Nice stuff, simply great!

I’ve recently started a site, the info you provide on this web site has helped me tremendously. Thanks for all of your time & work.

Thanks for all of your labor on this web site. Ellie take interest in setting aside time for investigations and it is simple to grasp why. A number of us hear all relating to the powerful form you provide practical items by means of this web site and in addition strongly encourage response from website visitors about this subject while my princess is now understanding so much. Have fun with the remaining portion of the year. Your carrying out a dazzling job.

There are certainly quite a lot of particulars like that to take into consideration. That is a nice point to bring up. I offer the ideas above as basic inspiration however clearly there are questions like the one you deliver up where the most important thing shall be working in sincere good faith. I don?t know if greatest practices have emerged around issues like that, however I’m positive that your job is clearly recognized as a fair game. Both boys and girls feel the affect of only a moment’s pleasure, for the rest of their lives.

This actually answered my downside, thanks!

Great web site. Plenty of helpful information here. I am sending it to some friends ans additionally sharing in delicious. And naturally, thank you in your sweat!

I’ve recently started a blog, the information you provide on this site has helped me greatly. Thank you for all of your time & work. “A creative man is motivated by the desire to achieve, not by the desire to beat others.” by Ayn Rand.

I am often to running a blog and i really recognize your content. The article has really peaks my interest. I am going to bookmark your web site and hold checking for brand spanking new information.

Hi! This is kind of off topic but I need some help from an established blog. Is it hard to set up your own blog? I’m not very techincal but I can figure things out pretty quick. I’m thinking about making my own but I’m not sure where to begin. Do you have any ideas or suggestions? With thanks

WONDERFUL Post.thanks for share..extra wait .. …

Aw, this was a really nice post. In thought I would like to put in writing like this moreover – taking time and precise effort to make a very good article… but what can I say… I procrastinate alot and not at all seem to get one thing done.

I like what you guys are up too. Such smart work and reporting! Carry on the excellent works guys I have incorporated you guys to my blogroll. I think it will improve the value of my site 🙂

Very interesting details you have observed, regards for posting.

I’m truly enjoying the design and layout of your blog. It’s a very easy on the eyes which makes it much more enjoyable for me to come here and visit more often. Did you hire out a developer to create your theme? Outstanding work!

Hmm is anyone else having problems with the images on this blog loading? I’m trying to figure out if its a problem on my end or if it’s the blog. Any feed-back would be greatly appreciated.

I do love the way you have framed this matter and it does indeed offer us a lot of fodder for thought. Nonetheless, coming from what I have observed, I simply hope when other opinions pack on that men and women remain on point and don’t get started on a tirade involving the news of the day. Still, thank you for this superb piece and although I can not concur with the idea in totality, I respect the viewpoint.

Hi, Neat post. There’s a problem with your site in internet explorer, would test this… IE still is the market leader and a big portion of people will miss your wonderful writing due to this problem.

910ta8

47wrlf

Hello there! Do you know if they make any plugins to safeguard against hackers? I’m kinda paranoid about losing everything I’ve worked hard on. Any tips?

z4wn4l